Data Center Liquid Cooling Market Trends Highlight Sustainability

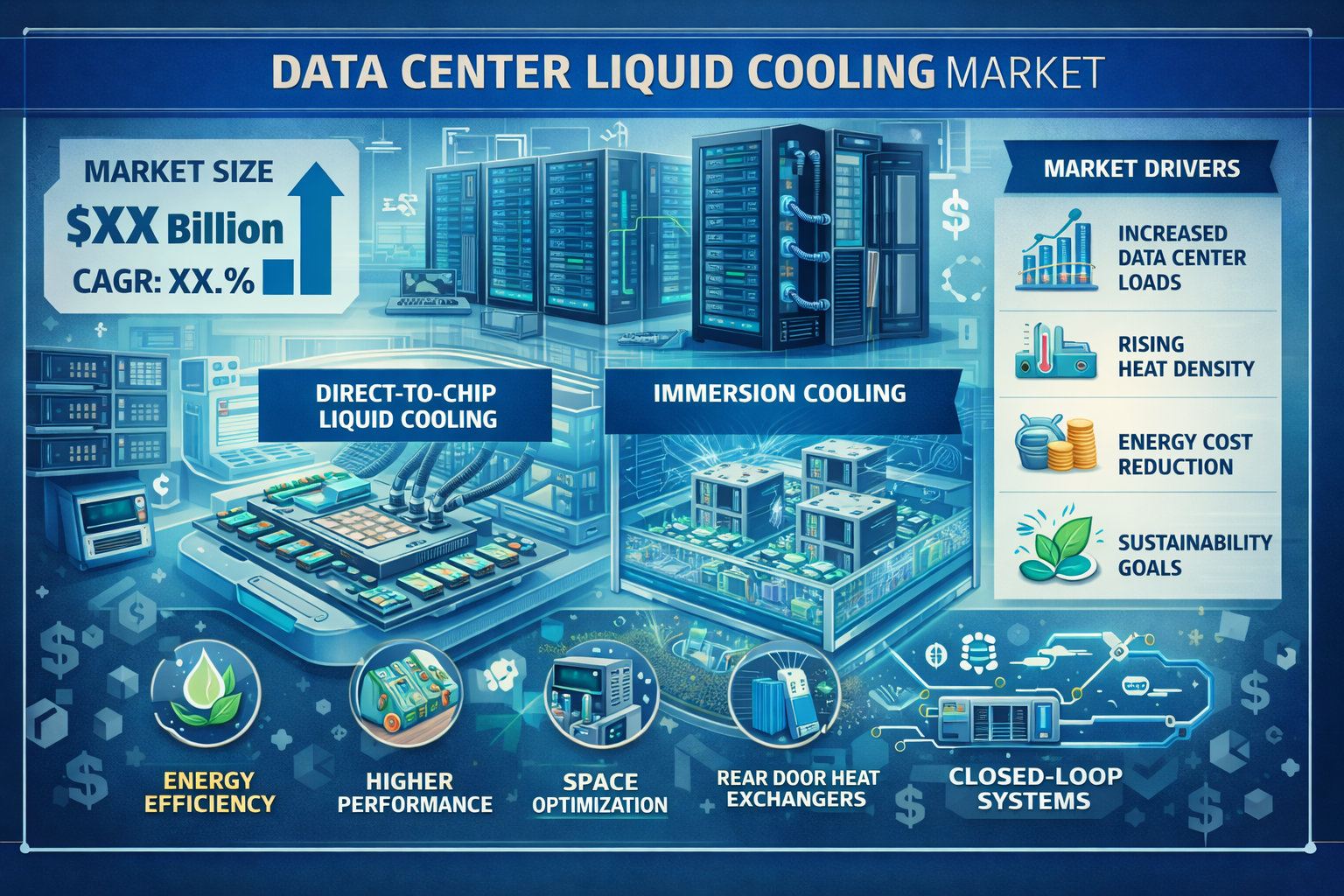

The global data center liquid cooling market is experiencing one of the most explosive growth trajectories in the entire technology infrastructure landscape. According to a published research report by The Insight Partners, the market is projected to surge from US$ 4,241.25 million in 2024 to US$ 22,079.85 million by 2031, registering a remarkable compound annual growth rate (CAGR) of 26.7% during the 2025–2031 forecast period. This exceptional expansion is being driven by the convergence of several transformative forces — the rapid proliferation of artificial intelligence workloads, the scaling of hyperscale data centers, the limitations of conventional air cooling at modern server densities, and the intensifying global imperative to reduce the energy consumption and carbon footprint of digital infrastructure.

Get the sample request - https://www.theinsightpartners.com/sample/TIPTE100000255

The Cooling Crisis at the Heart of the AI Era

To understand the data center liquid cooling market, it is essential to understand the thermal challenge that is redefining data center engineering. As AI model training, high-performance computing (HPC), and GPU-intensive workloads have become central to digital infrastructure operations, the heat generated per rack has increased dramatically — often far exceeding the thermal management capacity of traditional air-based cooling systems. Modern AI accelerator chips and high-density GPU clusters generate heat loads that air cooling simply cannot dissipate efficiently at scale, driving power usage effectiveness (PUE) metrics to unacceptable levels and creating the risk of thermal throttling that degrades compute performance.

Liquid cooling directly addresses this challenge by removing heat at or near the source with dramatically greater thermal efficiency than air. Whether through direct-to-chip cooling that circulates coolant through cold plates mounted on processors, or through full immersion cooling that submerges entire server boards in dielectric fluid, liquid cooling solutions can handle heat densities that are orders of magnitude beyond the limits of air cooling — while simultaneously reducing energy consumption, improving PUE, and enabling more compact, higher-density data center designs. As the AI infrastructure buildout accelerates globally, liquid cooling is rapidly transitioning from a niche, high-performance specialty to a mainstream requirement for competitive data center operations.

Key Market Drivers

Three primary drivers are propelling the market at its projected pace. The first is the urgent need to address high-density server cooling in AI, HPC, and hyperscale environments. As server densities increase and more heat is generated per unit of floor space, conventional air cooling systems are reaching the practical and economic limits of their effectiveness. Liquid cooling has become the preferred thermal management approach for these high-intensity computing environments, delivering precise temperature control and scalable performance that enables reliable operation of the most demanding workloads under continuous production conditions.

The second driver is the industry-wide push for energy efficiency and sustainability. Rising electricity costs, tightening environmental regulations, and growing corporate sustainability commitments are placing intense pressure on data center operators to reduce their energy consumption and carbon emissions. Liquid cooling systems consume significantly less electricity than equivalent air cooling infrastructure — primarily because moving heat in liquid requires far less energy than moving equivalent thermal loads through air — making liquid cooling a compelling tool for both operational cost reduction and sustainability target achievement. The ability of liquid cooling to improve PUE at scale is increasingly viewed as a strategic competitive advantage for cloud providers, colocation operators, and enterprise data center owners competing on operational efficiency.

The third driver is the continuous advancement of cooling technology itself. Innovations including immersion cooling, direct-to-chip solutions, modular cooling architectures, AI-driven adaptive cooling management, and IoT-enabled real-time monitoring are collectively expanding the performance envelope, economic accessibility, and operational manageability of liquid cooling systems. AI-powered predictive maintenance and building management system (BMS) integration are further enhancing the operational value of liquid cooling deployments by enabling proactive optimization and reducing unplanned downtime — critical capabilities for the hyperscale and colocation operators whose service-level commitments leave no margin for thermal incidents.

Market Segmentation

By cooling type, the market is divided into room-based, row-based, and rack-based cooling. Room-based cooling is suited to smaller server rooms and enterprise facilities with moderate heat loads, offering precise and energy-efficient thermal control for lower-density deployments. Row-based cooling systems, installed between server rows in medium- to large-scale data centers, provide a balanced approach to cooling capacity and energy efficiency well-suited for mid-density configurations, increasingly enhanced through IoT and AI-driven optimization. Rack-based cooling — encompassing direct-to-chip and immersion solutions applied at the individual rack level — represents the most intensive and technically advanced segment, directly addressing the thermal demands of AI accelerators, GPU clusters, and HPC nodes operating at the highest power densities achievable in modern computing infrastructure.

By data center type, the market spans hyperscale, colocation, wholesale, and enterprise data centers. Hyperscale data centers — operated by the world's largest cloud providers to power their global compute and storage infrastructure — represent the most demanding and technically advanced deployment environment for liquid cooling, and are a primary engine of market growth given the scale and pace of hyperscale infrastructure investment globally. Colocation data centers are rapidly adopting liquid cooling to accommodate the high-density AI and HPC workloads that enterprise customers are increasingly co-locating in third-party facilities.

By industry vertical, the market serves IT and telecom, BFSI, healthcare, manufacturing, government and defense, media and entertainment, retail, and energy sectors — a breadth of application that reflects the universal dependence of modern industry on data-intensive digital infrastructure.

Regional Landscape

Asia-Pacific is identified as the fastest-growing regional market, driven by the rapid digitalization of economies across China, Japan, India, and South Korea, the aggressive expansion of hyperscale data center capacity in these markets, and growing AI and HPC workload demands fueling investment in advanced thermal management solutions. North America remains the largest market by value, anchored by the massive concentration of hyperscale data center infrastructure operated by US-headquartered cloud providers and by the advanced state of AI infrastructure investment across the country. Europe's market growth is propelled by stringent energy efficiency regulations, strong sustainability mandates, and the large-scale deployment of high-density servers by cloud and enterprise operators in Germany, France, the Netherlands, and the United Kingdom. Emerging markets in Latin America, the Middle East, and Africa are also identified as growing opportunities as digital infrastructure investment accelerates in these regions.

Competitive Landscape and Recent Developments

Key players in the data center liquid cooling market include Asetek, Rittal GmbH, Stulz SpA, Carrier Global, Daikin Industries, Delta Electronics, Fujitsu, Mitsubishi, Schneider Electric, and Vertiv Group, alongside specialist innovators including CoolIT Systems, Green Revolution Cooling, Submer Technologies, LiquidStack, Iceotope Technologies, and Accelsius.

Two significant recent developments highlight the market's momentum. In November 2025, nVent Electric announced a new modular data center liquid cooling portfolio at SC25, including enhanced coolant distribution units and advanced technology cooling system manifolds aligned to current and future chip manufacturer cooling requirements. In September 2025, Schneider Electric unveiled a comprehensive end-to-end liquid cooling portfolio developed in partnership with Motivair, specifically engineered for hyperscale, colocation, and high-density environments to enable what the company describes as the AI Factories of the Future.

Conclusion

The data center liquid cooling market stands at the forefront of the infrastructure transformation being driven by the AI era. With the market projected to grow more than fivefold from 2024 to 2031 at a CAGR of 26.7%, liquid cooling represents one of the most compelling investment and commercial opportunities across the entire data center technology ecosystem — a market where the physics of heat dissipation, the economics of energy efficiency, and the strategic urgency of AI infrastructure are converging to make advanced thermal management not just desirable, but indispensable.

Related Reports

1 Data Center Air Cooling Market

About Us:

The Insight Partners is among the leading market research and consulting firms in the world. We take pride in delivering exclusive reports along with sophisticated strategic and tactical insights into the industry. Reports are generated through a combination of primary and secondary research, solely aimed at giving our clientele a knowledge-based insight into the market and domain. This is done to assist clients in making wiser business decisions. A holistic perspective in every study undertaken forms an integral part of our research methodology and makes the report unique and reliable.

Contact Us: If you have any queries about this report or if you would like further information, please contact us:

Contact Person: Ankit Mathur

E-mail: [email protected]

Phone: +1-646-491-9876